The Start-Up vs. The Corporation February 28, 2006

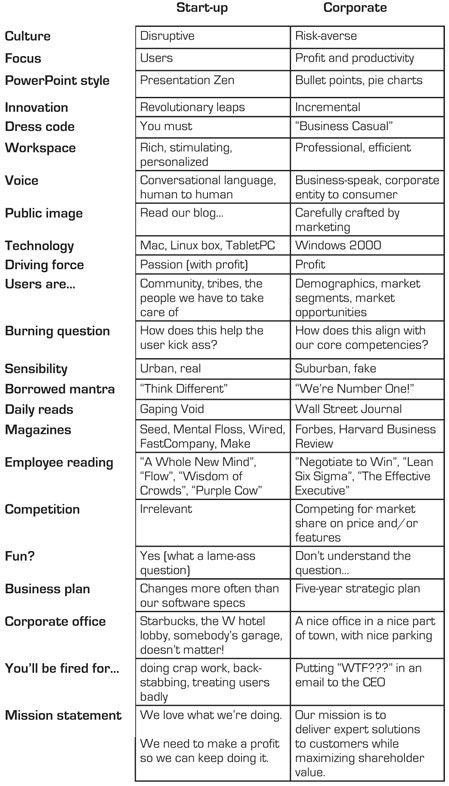

Kathy Sierra over at Creating Passionate Users created the chart below which illustrates the differences between the small start-ups we run, versus the large corporate powerhouses. An interesting point she made is that "When you evolve out of start-up mode and start worrying about being professional and dignified, you only lose capabilities. You don’t add anything…you only take away. Dignity is deadly."

I like to call them Hopeful Fibs January 9, 2006

This is a great article from Guy Kawasaki’s blog:

The Top 10 Lies of Entrepreneurs

1. “Our projections are conservative.” An entrepreneur’s projections are never conservative. If they were, they would be $0. I have never seen an entrepreneur achieve even her most conservative projections. Generally, an entrepreneur has no idea what sales will be, so she guesses: “Too little will make my deal uninteresting; too big, and I’ll look hallucinogenic.” The result is that everyone’s projections are $50 million in year four. As a rule of thumb, when I see a projection, I add one year to delivery time and multiply by .1.

2. “Gartner says our market will be $50 billion in 2010.” Every entrepreneur has a few slides about how the market potential for his segment is tens of billions. It doesn’t matter if the product is bar mitzah planning software or 802.11 chip sets. Venture capitalists don’t believe this type of forecast because it’s the fifth one of this magnitude that they’ve heard that day. Entrepreneurs would do themselves a favor by simply removing any reference to market size estimates from consulting firms.

3. “Boeing is going to sign our purchase order next week.” This is the “I heard I have to show traction at a conference” lie of entrepreneurs. The funny thing is that next week, the purchase order still isn’t signed. Nor the week after. The decision maker gets laid off, the CEO gets fired, there’s a natural disaster, whatever. The only way to play this card if AFTER the purchase order is signed because no investor whose money you’d want will fall for this one.

4. “Key employees are set to join us as soon as we get funded.” More often than not when a venture capitalist calls these key employees who are VPs are Microsoft, Oracle, and Sun, he gets the following response, “Who said that? I recall meeting him at a Churchill Club meeting, but I certainly didn’t say I would leave my cush $250,000/year job at Adobe to join his startup.” If it’s true that key employees are ready to rock and roll, have them call the venture capitalist after the meeting and testify to this effect.

5. “No one is doing what we’re doing.” This is a bummer of a lie because there are only two logical conclusions. First, no one else is doing this because there is no market for it. Second, the entrepreneur is so clueless that he can’t even use Google to figure out he has competition. Suffice it to say that the lack of a market and cluelessness is not conducive to securing an investment. As a rule of thumb, if you have a good idea, five companies are going the same thing. If you have a great idea, fifteen companies are doing the same thing.

6. “No one can do what we’re doing.” If there’s anything worse than the lack of a market and cluelessness, it’s arrogance. No one else can do this until the first company does it, and ten others spring up in the next ninety days. Let’s see, no one else ran a sub four-minute mile after Roger Bannister. (It took only a month before John Landy did). The world is a big place. There are lots of smart people in it. Entrepreneurs are kidding themselves if they think they have any kind of monopoly on knowledge. And, sure as I’m a Macintosh user, on the same day that an entrepreneur tells this lie, the venture capitalist will have met with another company that’s doing the same thing.

7. “Hurry because several other venture capital firms are interested.” The good news: There are maybe one hundred entrepreneurs in the world who can make this claim. The bad news: The fact that you are reading a blog about venture capital means you’re not one of them. As my mother used to say, “Never play Russian roulette with an Uzi.” For the absolute cream of the crop, there is competition for a deal, and an entrepreneur can scare other investors to make a decision. For the rest of us, don’t think one can create a sense of scarcity when it’s not true. Re-read the previous blog about the lies of venture capitalists, to learn how entrepreneurs are hearing “maybe” when venture capitalists are saying “no.”

8. “Oracle is too big/dumb/slow to be a threat.” Larry Ellison has his own jet. He can keep the San Jose Airport open for his late night landings. His boat is so big that it can barely get under the Golden Gate Bridge. Meanwhile, entrepreneurs are flying on Southwest out of Oakland and stealing the free peanuts. There’s a reason why Larry is where he is, and entrepreneurs are where they are, and it’s not that he’s big, dumb, and slow. Competing with Oracle, Microsoft, and other large companies is a very difficult task. Entrepreneurs who utter this lie look at best naive. You think it’s bravado, but venture capitalists think it’s stupidity.

9. “We have a proven management team.” Says who? Because the founder worked at Morgan Stanley for a summer? Or McKinsey for two years? Or he made sure that John Sculley’s Macintosh could power on? Truly “proven” in a venture capitalist’s eyes is founder of a company that returned billions to its investors. But if the entrepreneur were that proven, that he (a) probably wouldn’t have to ask for money; (b) wouldn’t be claiming that he’s proven. (Do you think Wayne Gretzky went around saying, “I am a good hockey player”?) A better strategy is for the entrepreneur to state that (a) she has relevant industry experience; (b) she is going to do whatever it takes to succeed; (c) she is going to surround herself with directors and advisors who are proven; and (d) she’ll step aside whenever it becomes necessary. This is good enough for a venture capitalist that believes in what the entrepreneur is doing.

10. “Patents make our product defensible.” The optimal number of times to use the P word in a presentation is one. Just once, say, “We have filed patents for what we are doing.” Done. The second time you say it, venture capitalists begin to suspect that you are depending too much on patents for defensibility. The third time you say it, you are holding a sign above your head that says, “I am clueless.” Sure, you should patent what you’re doing-if for no other reason than to say it once in your presentation. But at the end of the patents are mostly good for impressing your parents. You won’t have the time or money to sue anyone with a pocket deep enough to be worth suing.

11. “All we have to do is get 1% of the market.” (Here’s a bonus since I still have battery power.) This lie is the flip side of “the market will be $50 billion.” There are two problems with this lie. First, no venture capitalist is interested in a company that is looking to get 1% or so of a market. Frankly, we want our companies to face the wrath of the anti-trust division of the Department of Justice. Second, it’s also not that easy to get 1% of any market, so you look silly pretending that it is. Generally, it’s much better for entrepreneurs to show a realistic appreciation of the difficulty of building a successful company.

I’ve haven’t had the need for fundraising, yet, other than selling lemonade a decade or so ago hoping to overtake the Minute Maid empire. So some of these lies/truths would seem unapplicable to an entrepreneur such as myself as well as all of the other self-funded young go getters on this blog. But, I still think they are important points that are valid on a smaller level. We’ve all had to make that presentation at some point to a friend, parent, or colleague to get "venture capital", weather that be physical assets, emotional support, or a few spare bucks. So tell me whether or not you are willing to admit to letting one of these lies roll of your tongue in your young career.

Finding The Right Help

Through the ventures I’ve had of my own and through the experiences of my father, I can tell you that nothing can be done alone. Nothing of GREAT proportions anyways. Sure you can start a little biz focused on your little city with little room for growth and practically do it yourself, but you can’t build the huge empire you dream about all by your lonesome. Sooner or later you’re going to need to realize that not matter how smart, how effective, or how instinctive you are, you have areas where you could improve. But do you have time in your life to become an expert on everything? If you’re like most, you don’t have that luxury. You’re going to need to hire high-quality people to fill in the gaps and grow your business with you. We call these people ‘employees’ – and good ones are hard to find. Here are a few tips to help you on your quest for good help.

Only Heavy-Hitters

Don’t waste your time with people who just have some potential. Recruit those who have proven themselves in the past. If you only fill your positions with people who have proven they can play hard and play to win, you’re chances of success are phenomenal. Donald Trump says only recruit superstars. Heed his advice (this time!).

Keep A List

Through your networking events, business dinners, or even through small talk at the supermarket, you’re going to run into your heavy-hitters. Jot down their information and keep a running list of the top 5-10 (or more, depending on your organizations needs) people that you can possibly see yourself hiring or partnering with. Cultivate these relationships. Give them the attention they need to grow into something beneficial to you and your company.

Involve Them More

If you’ve successfully recruited a heavy-hitter and bypassed the guy that’s OK with 3 hots and a cot, you better be ready to involve them in the master plan. They’re not going to settle for monetary compensation because they know they’re worth more, and that’s OK – you know they are too. Show them your business plan. Show them your marketing plan. Ask for their suggestions and let them know that innovation from within the organization is OK and in fact is encouraged. Let them know that they can be as much a part of the company as they want to be, and that there’s no ceiling. A heavy-hitter won’t stay around if you clip their wings. You have to let them be creative and involve them in the growth of the company, not just in the filing and coffee making.

Bootstrapping with Rookies

OK, OK, this is a startup article. In many cases you might not have the funds to hire a heavy-hitter with a beautiful resume and references to match. That’s OK. It’s alright to hire a ‘rookie’ just on his enthusiasm and ‘potential’. This is more risky and not a sure bet, but if you can find someone with passion and intelligence and you use your gut instinct (yes, we’re back on that again) you’ll do fine. Entrepreneur’s have a gut reaction when they recognize a new opportunity or when they meet great people. Use that reaction to make the most informed decision possible.

You must have an extraordinary team to do extraordinary things with your company. You can’t do it all, so if you’re going to share the responsibility, share it with passionate, enthusiastic, intelligent individuals that will take pride in their work and strive to do right by you.

By Eric Windsor for YGG

Get Your Idea Going January 8, 2006

Plotting it out

I know, I know, it’s been said a million times over. I can’t stress enough how important a business plan is. Without one it’s the blind leading the blind. With the right plan you can prioritize your time and allocate your efforts and resources properly. Be careful, though; a plan is worthless if you don’t have the discipline to complete each step that you’ve outlined for yourself before moving on to the next item “to-do”.

Writing a business plan can be confusing; I highly suggest using Palo-Alto Software’s “Business Plan Pro” to help make the task easier and more concise. Check it out here: Business Plan Pro 2006

Clear your mind, clear the clutter

This is an entire topic on it’s own which I will touch on next week, but I have to mention it. Your time, money and creative energy is precious, especially during the startup phases. Try to eliminate the procrastinating tasks (we all have them) that occupy too much of your time. Do you really need to check your E-mail 10 times an hour (or more?). If it’s important enough, they’ll call you. Do you really need to check your bank balance that often? Do you need to change your desktop wallpaper everyday? Eliminate the unimportant tasks and focus on the things that are going to make your dreams come true.

Follow your gut

Ditch the distractions and listen to your gut instinct. If you’re a serious entrepreneur and you’re serious about building your business and growing your idea, you can feel decisions in your gut before you make them. Go with it. No one ever got anywhere by over analyzing. Focus your energy on defining your business and personal goals, know what you want, and let your entrepreneurial instinct take you to the finish line. Evaluate what’s a distraction and what’s really going to get you from point A to point B. If you’re feeling distracted, take some quiet time to yourself, ask yourself (out loud helps) what you should be doing right now instead of procrastinating and I promise you’re gut instincts will lead the way.

I know this is somewhat of a motivational type post, but we all need it sometimes. Ring in 2006 the right way and get focused. Start building the life you desire today, not tomorrow.

Why Small Businesses Fail December 31, 2005

The SBA says 50% fail during first year

The U.S. Small Business Administration has seen lots of small businesses come and, unfortunately, go. According to the SBA, over 50% of small businesses fail in the first year and 95% fail within the first five years. Why? What goes wrong?

In his book Small Business Management, Michael Ames gives the following reasons for small business failure:

1. Lack of experience

2. Insufficient capital (money)

3. Poor location

4. Poor inventory management

5. Over-investment in fixed assets

6. Poor credit arrangements

7. Personal use of business funds

8. Unexpected growth

9. Competition

10. Low sales

These figures aren’t meant to scare you, but to prepare you for the rocky path ahead. Underestimating the difficulty of starting a business is one of the biggest obstacles entrepreneurs face. However, success can be yours if you are patient, willing to work hard, and take all the necessary steps.

On the Upside

It’s true that there are many reasons not to start your own business. But for the right person, the advantages of business ownership far outweigh the risks.

You will be your own boss. Hard work and long hours directly benefit you, rather than increasing profits for someone else. Earning and growth potential are far greater. A new venture is as exciting as it is risky. Running a business provides endless challenge and opportunities for learning.

Source: U.S. Small Business Administration

Is Entrepreneurship For You?

Are you ready?

In business, there are no guarantees. There is simply no way to eliminate all the risks associated with starting a small business - but you can improve your chances of success with good planning, preparation, and insight. Start by evaluating your strengths and weaknesses as a potential owner and manager of a small business. Carefully consider each of the following questions.

Are you a self-starter?

It will be entirely up to you to develop projects, organize your time, and follow through on details.

How well do you get along with different personalities?

Business owners need to develop working relationships with a variety of people including customers, vendors, staff, bankers, and professionals such as lawyers, accountants or consultants. Can you deal with a demanding client, an unreliable vendor, or a cranky receptionist if your business interests demand it?

How good are you at making decisions?

Small business owners are required to make decisions constantly - often quickly, independently, and under pressure.

Do you have the physical and emotional stamina to run a business?

Business ownership can be exciting, but it’s also a lot of work. Can you face six or seven 12-hour work days every week?

How well do you plan and organize?

Research indicates that poor planning is responsible for most business failures. Good organization of financials, inventory, schedules, and production can help you avoid many pitfalls.

Is your drive strong enough?

Running a business can wear you down emotionally. Some business owners burn out quickly from having to carry all the responsibility for the success of their business on their own shoulders. Strong motivation will help you survive slowdowns and periods of burnout.

How will the business affect your family?

The first few years of business startup can be hard on family life. It’s important for family members to know what to expect and for you to be able to trust that they will support you during this time. There also may be financial difficulties until the business becomes profitable, which could take months or years. You may have to adjust to a lower standard of living or put family assets at risk in the short-term.

Courtesy of the Small Business Administration www.sba.gov